Detailed analysis of trident techlabs

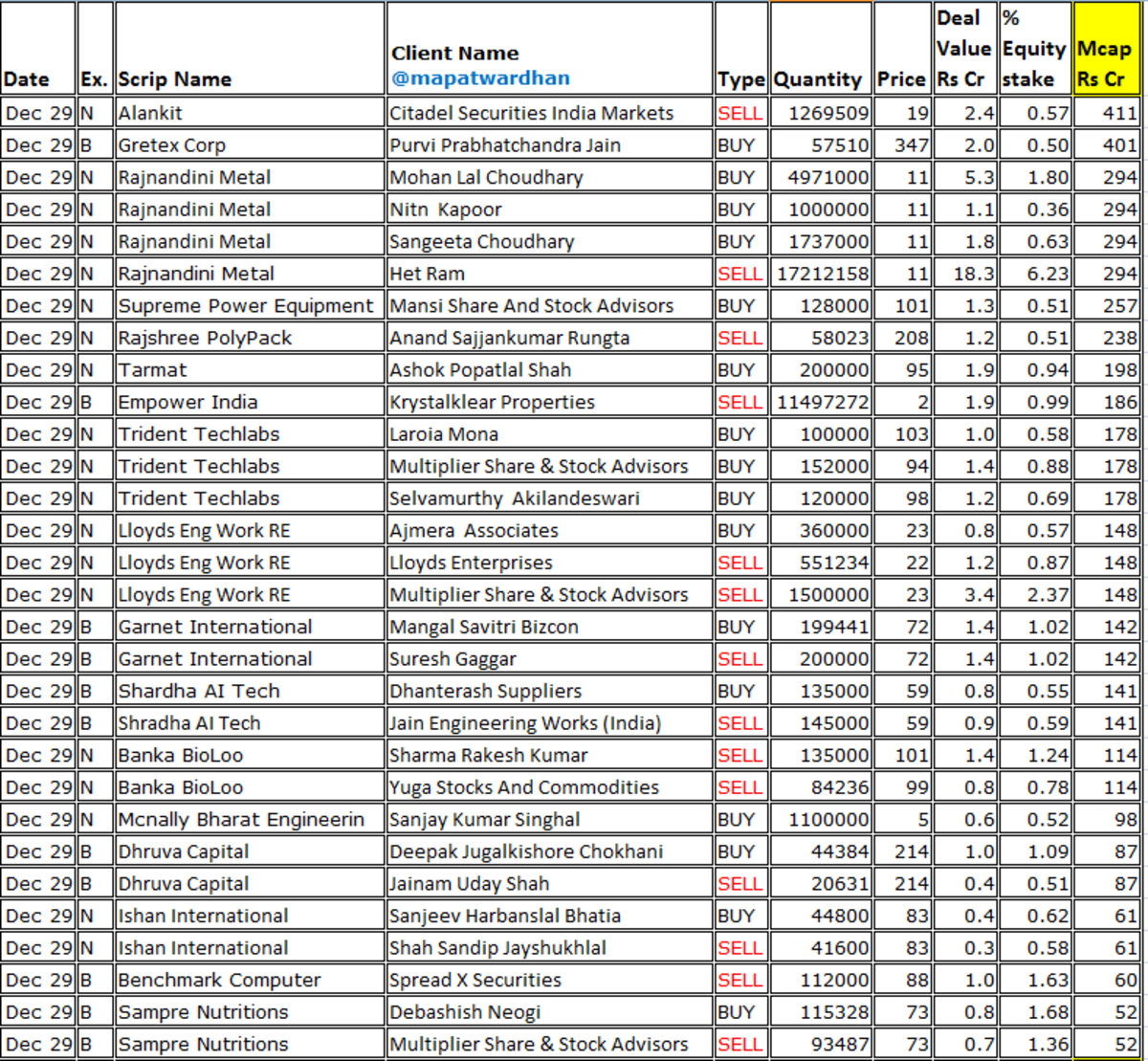

📌BULK deals update:-

➢SELVAMURTHY AKILANDESWARI Bought 1.2L shares at Rs.98.15.🔥

➢LAROIA MONA bought 1L shares at Rs.103.04.🔥

📌FY24:- 7 Month PAT: 2.66Cr

➡️FY24 expected PAT is 12-13Cr🔥 (based on industry information and investor chatter)

📌Promoter was classmate of AJIT DOVAL 😮🔥 (National Security Advisor of India to Prime Minister Narendra Modi)

( INFO is heard from the street, this info can be completely wrong, pls do your due diligence)

📌📌 ➡️ ➡️

▪️Incorporated in 2000, Trident Techlabs Limited✅ provides technology-based solutions to the Aerospace🚀, Defense, automotive, telecommunications, semiconductor, and power distribution industries.

▪️It provides tailor made engineering and power system solutions to its customers.💫

📌The company has two verticals:-

▪️1)Engineering Solutions:- Consulting and technical services in system-level electronic design, chip-level electronic design, embedded design, hydraulic/pneumatic systems, system modeling, reliability and quality, design automation, power electronics, PCB design, and electromagnetic simulations.✅

➢Its design services include consulting and engineering services that help companies innovate better, with services spanning the entire product development lifecycle, including strategy and user research, design and engineering, pre-launch testing and post-launch maintenance, and service delivery and optimization. 🔥

▪️2)Power System Solutions:- providing products and services to power distribution utilities that help them maximize the capacity of aging transmission infrastructure, manage increasing intermittent generation from renewable energy sources, and deploy smart grid technologies that add complexity to transmission investment decisions.✅

➢TTL's solutions and services dwell on the latest technology to enable clients in maximizing the reliability of their electric power facilities in the most economical manner. 🔥

▪️The company delivers winning business outcomes through its deep industry experience and a 360-degree view of "Business through Technology" helping clients in creating successful and adaptive businesses.💫

📍➡️Their USP in Engineering Solutions:-

➢Broadest range of design tools which allows selection of tool optimal for a given application area.💫

➢Best-in-class design tools at affordable prices.✅

➢Top-end technical support to the users on how to best use the design tool.

📍➡️Their USP in Power Solutions:-

➢Best-in-class analysis tools.✅

➢Tool-based analysis of safety of installed equip & operating personnel.

➢Services for preparation of requested database and computer model of network.

▪️The Company has business alliances with the OEMs of various computer-aided engineering tools, from whom these tools are sourced by Company and supplied to the market in India in with a variety of value-added services, ranging from training on usage of the tool, its maintenance in the IT ecosystem of the users, its application to real-life projects as well as on-site deployment of manpower for accomplishment of client's projects, in part or total, etc.

➢Trident Techlabs employs more than 100 engineers and professionals.

📌📌

▪️IPO price: Rs.35

▪️IPO size: 16.03CR

▪️CMP:Rs.113

▪️Market cap:196 CR

▪️P/E:43 (annualized)

▪️52 Wk High: 113.6

▪️52 Wk Low: 93.25

▪️ROE: 34.41%

▪️ROCE: 23.67%

▪️RoNW: 29.36%

▪️Debt/Equity: 0.84

▪️Assets:61.44Cr

▪️Total Borrowing:25.32Cr (Reserves and Surplus:12Cr)

▪️Share Holding Pre Issue:92.48%

▪️Share Holding Post Issue:67.97%

📌FINANCIALS:

▪️FY24:-7 Month Rev: 21.14Cr

▪️FY24:-7 Month PAT: 2.66Cr

▪️FY23 revenue is 68.24Cr as compared to 29.87 CR(FY22), 128 %✅ growth yoy.

▪️FY23 PAT is 5.54 CR as compared to 0.645 CR(FY22), 758%✅ growth yoy.

▪️140% growth in revenue in last 2 years.

(PAT margins of 0.59% (FY21), 2.20% (FY22), 8.24% (FY23), 12.66% (M7-FY24)✅)

▪️Revenue from India :98-99%

▪️Revenue outside India: 1-2% (South-East Asia, Middle East, China, Bangladesh and Sri Lanka etc)

📌IPO funds:

From the net proceeds of the IPO funds, it will utilize Rs. 12.00 cr. for working capital, and the rest for general corporate purposes.

📌PEERS:

As per offer document, the company has no listed peers to compare with.

(In CRISIL report they have shown SIEMENS INDIA and ETAP(US) as peers)✅

📌SECTOR GROWTH:

▪️Government's outlay for the power sector has increased by 24% for fiscal 2024 over the revised estimates of fiscal 2023 whereas infrastructure related spending has increased by 17% as per the latest union budget.💫

▪️CRISIL Research projects investments of Rs 25.5-26 trillion in the power sector in six years.✅

▪️Railway electrification, Govt initiatives, Transition to Grid, Transition to EV.(Power demand will rise)

▪️As per Engineering Services global Market 2023, the global engineering services market size will grow from $1,110.21 billion in 2022 to $1,156.5 billion in 2023 at a compound annual growth rate (CAGR) of 4.2%. and expected to grow to $1,316.06 billion in 2027 at a CAGR of 3.3%.✅

▪️The E-learning market in private schools is anticipated to increase by 35-40% CAGR between fiscal years 2022 and 2025.✅

📌STRENGTH:

➢Wide product portfolio of customized products, tools and services.💫

➢360-degree knowledge and experience of various industries.✅

➢Strong relationship with a diverse customer base.

➢Strong and customer centric support services provided in the Engineering and Power Systems Solutions space.

➢Experienced Promoters and senior management team.

📌FUTURE PLAN:

▪️Further expanding their services into the international markets.✅

▪️Expansion of their Power Systems Solutions portfolio💫

▪️Further expansion and enhancement of their Engineering Solutions in the defence and aerospace sector.🚀🚀

▪️Focus on increasing revenues by leveraging core competencies and grow their business.

▪️Continue to enhance their core strengths by attracting, retaining and training qualified personnel

📌Disclosure: Not a buy recommendation ,only for study and education purpose. Please consult your financial advisor before investing. Please stop investing blindly. I have no investment in it.🙏

RHP

RHP