Indias largest white oil player One of the top 5 player globally Large scale of operations backed by solid and consistent financial and balance sheet track record 53% rev from exports Focus on speciality oil segment with enhanced scale of operations PHPO: Fastest growing segment and largest business division 54.6% rev in FY23 White Oil is fastest growing segment with CAGR of 9.9% expected between FY23-28E Industry leading RoE and RoCE with 32.2% and 41.1%???? PHPO: Time of empanelment can take up to 4-5years Big moat Largest segment with fastest growth FY21-23: Rev CAGR of 64.9%???? Volume growth CAGR of 28.52% Cosmetics and healthcare formed 69.34% of overall revenue To expand into contract manufacturing services In the process of enhancing production capacity Taloja plant: To add 1,00,000 kl by FY24???? Silvassa plant: To add 18,840 kl(Automotive oils) #Q2FY24: APAC and Americas continue to witness strong demand Favorable industry trends for consumer and healthcare segments Positive outlook for overall business Steady gross margin spread for last 3years Q2 had a steady spread too H2 is stronger vs H1 due to winter falling in H2 Q2 is weak qtr due to it being monsoon qtr However, there now no comparable nos given for #Q2FY24 vs #Q2FY23 and #H1FY25 vs #H1FY23 First concall on Tuesday 11am

Results are flat and average as the revenue was the key point here, because we don't have previous data to compare with. Companies generally do this to avoid decline in stock price. I'm expecting 8-10% fall. Price should hold in between, 250-270. Still a cheap valuation at current levels, but to be fair many have kept SL at lower levels to avoid loosing listing gains. Monday 270-275.

concall with the management on 19.12.23 at 11.00 AM, will clear regarding company future growth, so wait till then. The crude oil was the villain in last quarter(due to gaza Isreal conflict). Now wait for the upcoming quarter results, as now it's (crude) stabilized.

362.2. R.A.| Link| Bookmark|

December 16, 2023 7:34:35 PM

Top Contributor (300+ Posts, 100+ Likes)

@Monster Zero You must understand here one thing that company is working at it's 95% capacity. So flap results were expected and it will be continued untill new plant starts till March 2024. So growth story will be shown from FY 2025 financials. Company have almost fix margins for the product. Prices may very depending on the global situation. In my opinion price movement would not be due to results. There may be other reasons for it

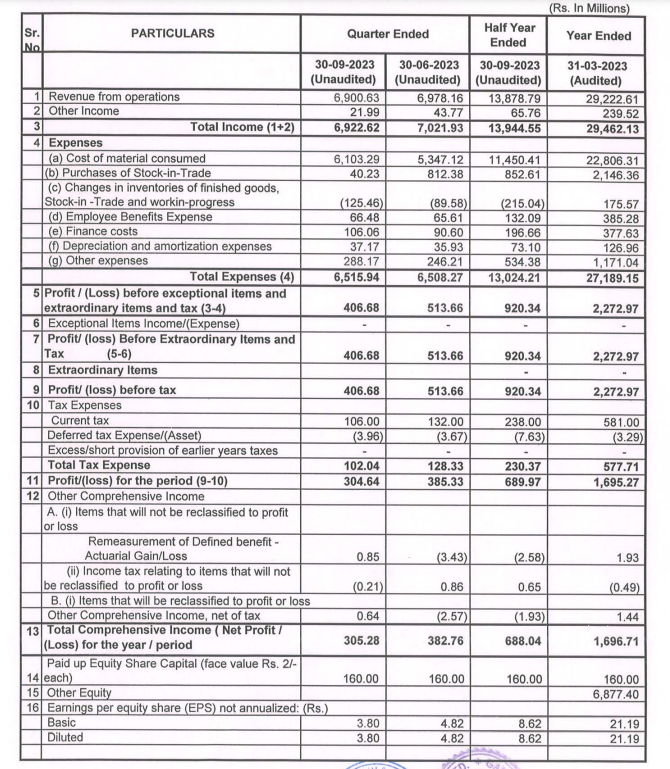

@newgen consultancy Gandhar has posted 48 Cr PAT for Sep 23 quarter and 102 Cr for the half year ended Sep 23. As we don't have data to compare this with previous year, please explain your opinion on the results whether they are good. Also please tell whether we can hold this. Thanks in advance06

361.1. CoolAsh| Link| Bookmark|

December 15, 2023 8:49:39 PM

Top Contributor (700+ Posts, 100+ Likes)

@Sandy I see different numbers at BSE website and the funny thing is that the June 23 numbers posted at CG are not matching what we have at BSE website. I am totally lost here

360. CoolAsh| Link| Bookmark|

December 15, 2023 5:52:52 PM

Top Contributor (700+ Posts, 100+ Likes)

Results are out

QoQ EPS dipped from 4.82 to 3.8. Cost of raw materials increased from 534 crores to 610 crores leading to a dip in QoQ profits from 38 crores to 30 crores. Top line is flat QoQ. I think we will need to wait for the Dec 23 results

354.1. CoolAsh| Link| Bookmark|

December 5, 2023 9:04:51 PM

Top Contributor (700+ Posts, 100+ Likes)

This may stay range bound till we have Sep 23 results and maybe till Dec 23 results as well. However, there are reasons to be optimistic in the next 6 months or so. We can see a move up to 400 in 3-6 months time IMO.

353. CoolAsh| Link| Bookmark|

December 5, 2023 11:11:43 AM

Top Contributor (700+ Posts, 100+ Likes)

Do we know if the September 23 results have been declared by Gandhar?

Sir, All the best for your endeavour. But, I am sorry to express my view that the price may not fall to that stage of Rs.200/- in near future in the present circumstances. Extremely sorry.

349.2. CoolAsh| Link| Bookmark|

December 3, 2023 3:21:41 PM

Top Contributor (700+ Posts, 100+ Likes)

Agree. I don't think there will be much further fall now. Looking at election results it may even rebound above 300

@DSR ji.. You have bought Gandhar..at a reasonable price.. In my openion price will not fall below 240-250..I was also not allotted it.. & have bought it at the range of 290..280..& will add more at 260..250..240..this is a strong candidate to give 25-30℅ profit in very near future.. I may be totally wrong.. This is only my View.. No guaranty.. No claim.. because share market works on his own way.. all logics can be failed here.. Best of luck to you for your all future investments.. Sir

@KSRK.. Brother I read somewhere that 2 qtr result of Gandhar are to be declare on 15 Dec.. so be aware & keep watching results.. Hope you will get profit in Gandhar.. I also purchased 150 @ 272-275 range

Kapoor ji, Very kind of you. Thank you very much for your sweet n affectionate words with concern. I shall be ever grateful to you. I pray God to bless you with all the best. Please continue to shower your kind blessings to this brother.

Now since the results are flat.. we have seen immediate reaction as well on the stock price and a sharp recovery.. but I was hoping a little more correction.

I intend to add more below 240 only. So holding my position as of now.

348. UjwalG| Link| Bookmark|

December 1, 2023 1:01:46 PM

IPO Guru (1300+ Posts, 600+ Likes)

@Vimal Garodia Ji, sorry for disturbing. Whats the retal quota in buyback? 15% right? Or 35% of total issue size. Cant remember exactly

SIS Lts. is a good one to opt for at CMP. There will not be much downfall for the unaccepted shares after the buyback. AR will also be around 40%. Of course, you may be aware of all these things.

It's true competitors are Panama petro and Savita oil they are currently trading at 10-13 pe ... I don't hope that it can make wonders... In my opinion it's true value is around 23x12=276.... Your comments for this is welcome

RHP

RHP